Futures Market: Overnight, LME copper opened at $9,134.5/mt, rose slightly at the beginning of the session, then fluctuated downward, hitting a low of $9,103.5/mt. It subsequently climbed throughout the session, reaching an intraday high of $9,185/mt, but the center slightly declined towards the end, closing at $9,174/mt, up 0.7%. Trading volume reached 15,000 lots, and open interest stood at 282,000 lots. The most-traded SHFE copper 2503 contract was closed overnight.

【SMM Copper Morning Brief】News: (1) On February 1, US President Trump signed an executive order to impose a 10% tariff on goods imported from China. According to the order, the US will also impose a 25% tariff on goods imported from Mexico and Canada, with a 10% tariff specifically on Canadian energy products.

(2) With approval from the State Council, China will impose tariffs on certain US-origin imported goods starting February 10, 2025. A 15% tariff will be applied to coal and liquefied natural gas, while crude oil, agricultural machinery, large-displacement vehicles, and pickup trucks will face a 10% tariff.

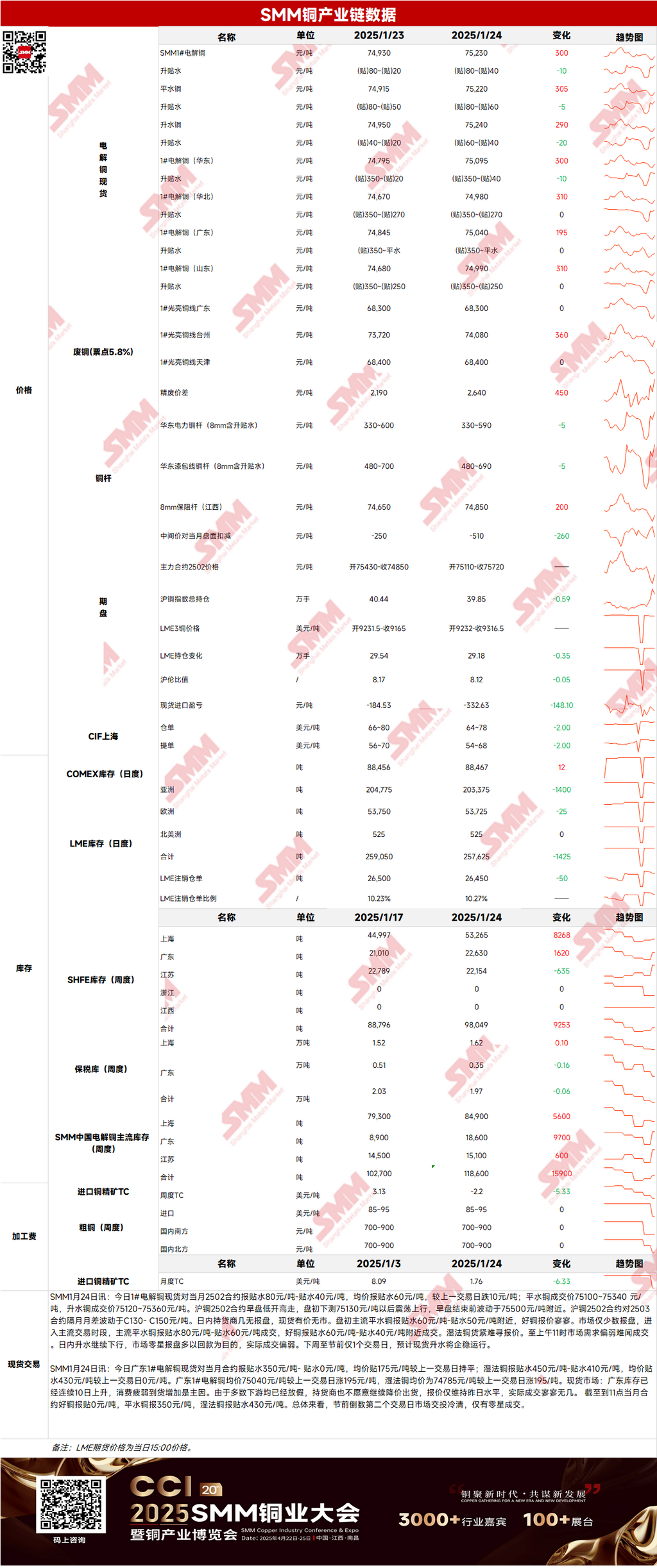

Spot Market: (1) Shanghai: On January 27, mainstream standard-quality copper spot prices against the front-month contract were quoted at a discount of 70-50 yuan/mt, while high-quality copper was quoted at a discount of 40-20 yuan/mt. According to SMM, significant inventory buildup has already begun in east China this week, with the market showing prices but no transactions before the Chinese New Year.

(2) Guangdong: On January 27, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 260-0 yuan/mt, with an average discount of 130 yuan/mt, up 45 yuan/mt from the previous trading day. Hydro copper was quoted at a discount of 360-320 yuan/mt, with an average discount of 340 yuan/mt, up 90 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 75,090 yuan/mt, up 50 yuan/mt from the previous trading day, while hydro copper averaged 74,880 yuan/mt, up 95 yuan/mt. Overall, pre-holiday sentiment was strong, and market trading was quiet, with suppliers mainly registering warehouse warrants.

(3) Imported Copper: On January 27, warehouse warrant prices were $64-78/mt, QP February, with the average price unchanged from the previous trading day. B/L prices were $54-68/mt, QP February, with the average price unchanged from the previous trading day. EQ copper (CIF B/L) was quoted at $4-18/mt, QP February, with the average price unchanged from the previous trading day, referencing cargoes arriving in early to mid-February. Pre-holiday SHFE/LME price ratio improved, but most market traders had already gone on holiday, leaving the US dollar-denominated copper market quiet.

(4) Secondary Copper: On January 27, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 68,200-68,400 yuan/mt, unchanged MoM. The price difference between primary metal and scrap was 2,705 yuan/mt, up 65 yuan/mt MoM. The price difference between primary metal and rod was 1,020 yuan/mt. According to the SMM survey, there were almost no transactions in the market, and enterprises indicated that copper prices were hovering around 75,000 yuan/mt during the holiday, with potential for an upward trend after the holiday.

(5) Inventory: On January 27, LME copper cathode inventory decreased by 1,800 mt to 255,825 mt. On the same day, SHFE warehouse warrant inventory increased by 3,600 mt to 25,445 mt.

Prices: Macro side, the US previously delayed imposing tariffs on goods from Mexico and Canada, easing trade tensions. However, concerns over trade tensions and global economic growth persisted. Meanwhile, US job vacancies hit their lowest level since September last year, and December factory orders recorded the largest monthly decline since June 2024. Weak data led to a weaker US dollar, providing some support to LME copper. However, gains were limited due to concerns over demand. Fundamentals side, pre-holiday copper social inventories increased, and downstream enterprises indicated that many would start operations later or had pre-holiday stockpiling for post-holiday production. Overall, consumption recovery remains to be seen. On the first trading day after the holiday, copper prices are expected to see limited gains.

》Click to view the SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】